Many of us have watched interest rates rise and fall like a rollercoaster ride, and I must say, it’s been more entertaining than my last trip to the dentist! Just the other day, I noticed that the 6-month T-bill yield in Singapore has plummeted to around 27%. It got me thinking about my own experience with investments and the quirks of finance, like that time I thought I’d outsmart the market only to end up with more regrets than profits. So, let’s examine the reasons behind this dip in T-bill rates, shall we?

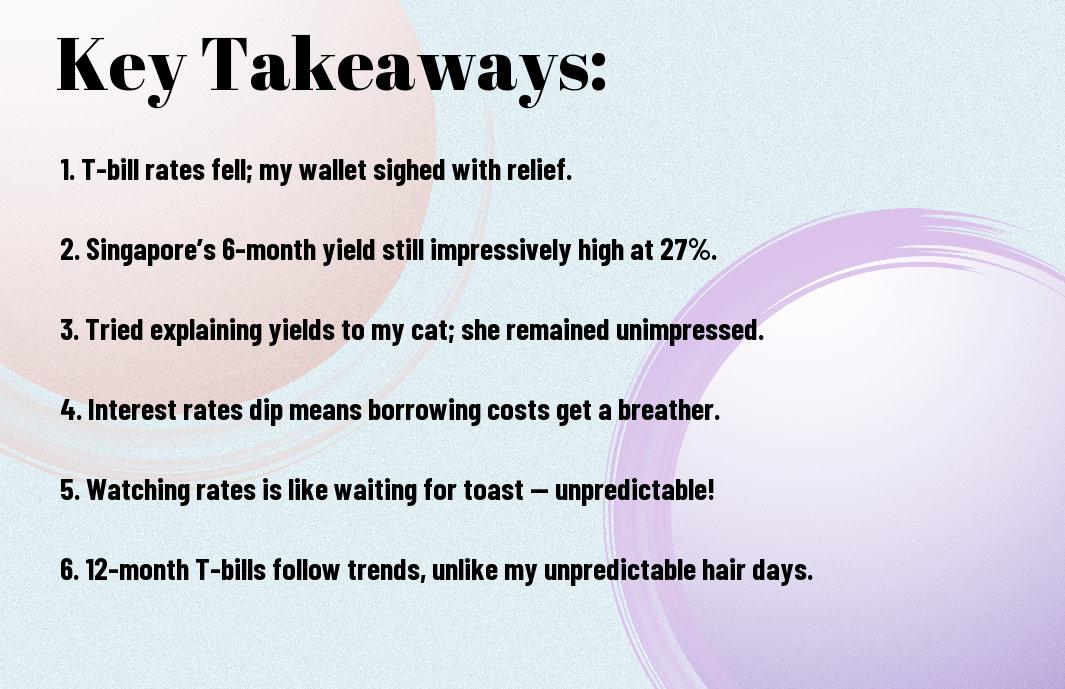

Key Takeaways:

- The recent dip in T-bill interest rates can be attributed to a global trend of central banks adjusting their monetary policies. It’s like when your favourite café downsizes its coffee sizes because they ran out of cups – it’s frustrating but sometimes necessary!

- Market sentiment plays a significant role in T-bill yields. Investors might be feeling rather optimistic, as if they’ve just won a game of poker, leading to lower yields. It’s all fun and games until someone loses their chips – or in this case, their interest rate!

- In Singapore, the 6-month T-bill yield is currently at a staggering 27%. It’s almost as outrageous as the price of ordering a pint in a Wetherspoons on a Friday night! You pay for what you get, I suppose!

- Economic indicators such as inflation and unemployment rates affect T-bill yields. Just like when you’re trying to convince your mate to pay for the next round – if the economy’s a bit dodgy, interest rates are a bit dodgy too!

- Investing in T-bills can be likened to dating – sometimes you get a good return, but other times you just end up in an awkward situation. Just last week, I thought I landed a decent date, only to discover they were a complete bore – much like an underperforming bond!

What Are T-Bills?

The term T-bill, or treasury bill, may sound like a fancy dinner guest, but they’re actually short-term government securities that you can purchase to lend money to the government. Unlike that dinner partner who hogs the conversation, T-bills take only a few months to mature, making them a relatively quick investment. They’re known for being low-risk, but don’t get your hopes up for wild returns!

T-Bills Explained

With T-bills, you’re vitally buying a promise from the government to pay you back in a very short time – usually up to a year. You purchase them at a discount, meaning you’ll receive the full face value upon maturity. If only everything else in life were as straightforward! You give them a bit of cash, and they promise to give you back more… eventually.

The Basics of T-Bill Interest Rate

With interest rates, things can get a bit playful, like your favourite game of hide and seek! They can fluctuate over time based on a range of economic factors that even the most astute among us may find baffling. It’s like trying to predict British weather – sunny one minute, pouring the next!

Interesting Posts

Indeed, interest rates can significantly impact your investment choices, including T-bills. When rates rise, newly issued T-bills come with better yields, enticing investors like me to hop on board instead of sticking with the older, lower-yield ones. It’s like being lured away by a tastier dessert on a buffet table. I mean, who can resist that? Understanding these shifts helps you make better financial decisions, potentially boosting your overall returns in the long run. Just don’t forget to keep a good eye on those pesky fluctuations!

The Recent Drop in T-Bill Interest Rates

If you’ve been keeping an eye on the T-bill interest rates, you might have noticed a rather surprising drop recently. I mean, one minute they’re flying higher than your morning coffee buzz, and the next, they’re tumbling down like a toddler on a sugar crash! It’s a bit like taking a wild ride on a rollercoaster – just when you think you’re on a high, the ground is suddenly closer than you anticipated.

Factors Contributing to the Decline

Behind every drop in interest rates, there are reasons galore that keep economists scratching their heads. It’s like watching a magician pull a rabbit out of a hat—how do they do it? Here are some factors I’ve observed:

- Market fluctuations

- Changing economic forecasts

- Inflation expectations

- Monetary policy adjustments

Assume that the economy is taking a breather, and financial wizards are casting their spells on those rates.

Comparing T-Bill Rates Over Time

Among the many interesting aspects of T-bill rates is how they fluctuate over time. It’s as if they have their own seasonal wardrobe. Here’s a snapshot of how things have changed:

| Year | 6-Month Yield |

|---|---|

| 2020 | 1.20% |

| 2021 | 0.85% |

| 2022 | 0.45% |

| 2023 | 0.27% |

As you can see, T-bill rates seem to shift like a chameleon, adapting to conditions and expectations over time. It leaves some of us wondering whether we need a crystal ball to keep up!

Another intriguing observation is that the context of these rates can sometimes tell a more comprehensive story – one that encompasses not just numbers but sentiments and probabilities.

| Year | 12-Month Yield |

|---|---|

| 2020 | 1.50% |

| 2021 | 1.00% |

| 2022 | 0.65% |

| 2023 | 0.35% |

It’s evident that these rates can evoke a myriad of responses, as the financial winds change direction. Here’s hoping we all keep our balance, consuming enough tea, to ride the financial waves with a good dose of humour!

Personal Experiences with T-Bill Interest Rate

Keep in mind that my adventures with T-Bills have been quite the ride! From the first time I stumbled into the world of Treasury Bills to the moments of sheer confusion and hilarity that ensued, I’ve got stories that will make you chuckle. Just when I thought I’d cracked the subtle art of investing, life threw a few curveballs my way, reminding me that learning can sometimes feel like more of a comedy sketch than a financial seminar!

My First T-Bill Investment: A Comedy of Errors

Beside my attempt at adulting, my inaugural foray into T-Bills was a prime example of “what not to do.” Picture me sorting through a mountain of financial jargon, convinced I’d struck gold with a great investment, only to discover I’d accidentally signed up for a holding period longer than one of my failed New Year’s resolutions. It was as if the universe was chuckling at my expense!

The Time I Thought I was a Financial Guru

Below that moment of enlightenment was when I truly believed I’d become a financial prodigy. Armed with a spattering of knowledge from YouTube videos (one too many “How to Invest” tutorials), I strutted around my local café, confidently telling anyone who’d listen about the wonders of T-Bills. Maybe I should’ve just stuck to ordering my flat white instead.

In fact, I had read so much about T-Bills that I felt like a Wall Street whiz kid! I even tried to impress my friends with my newfound jargon, insisting they join me in buying, much to their confusion. They probably thought I was running some sort of financial cult. Spoiler alert: it wasn’t a cult, just me realising that knowing the difference between yield and yield curve was as baffling as deciphering a toddler’s drawing!

Understanding the Current Yield in Singapore

After countless afternoons spent sipping kopi and pondering the mysteries of T-bills, I’ve finally grasped the current yield situation in Singapore. The 6-month T-bill yield hovering around 27% feels like winning the lottery—if only I had actually bought that ticket! With yields this spicy, it seems I’m not the only one racing to snatch up these attractive rates, making my understanding of T-bills far less theoretical than before.

What Does a 27% Yield Mean?

Beside the fact that a 27% yield sounds like a number pulled straight from a finance fairy tale, it actually represents a lucrative investment opportunity. If you invest, say, a grand, you’re looking at a return that could make your wallet fatter than a Singaporean hawker centre meal! Just imagine what I could do with all that extra cash—perhaps even afford a taste of those famed chilli crabs.

Contextualizing Singapore’s T-Bill Market

What makes Singapore’s T-bill market so intriguing is its stability amidst the fluctuating financial waves. Here, T-bills aren’t just paper; they’re golden tickets to a promised land of secure returns. The bustling economy and strong government backing underpin these financial instruments, making them a favourite for both seasoned investors and newcomers like me, who are eager to dip a toe in the investment waters.

Consequently, Singapore’s T-bill market has become a beacon for those seeking safety and decent returns, especially in uncertain times. I, for one, feel encouraged by the competitive yields, leading me to contemplate my own investment strategies. It’s as if the market were shouting at me: “Invest wisely, and the rewards could be more satisfying than a plate of char kway teow!”

Humorous Anecdotes Related to T-Bill Interest Rate

All of us have those moments when we speak about finance, and everyone suddenly looks like they’ve seen a ghost. At my friend’s party, I attempted to explain T-Bills while balancing a drink in my hand. All I can say is, the cocktail didn’t mix well with the numbers, and before long, I was comparing the yield on T-Bills to cooking spaghetti. I might have also suggested investing in ‘noodles’ instead because they were ‘al dente’. You could practically hear the crickets chirping!

When I Tried to Explain T-Bills at a Party

After what I thought was a grand opening line about short-term investments, I realised my audience’s eyes were glazing over faster than a doughnut! I valiantly pressed on, but each technical term just led to more confusion. By the end, my friends were convinced I was trying to sell them a used car instead of explaining a financial instrument. I might as well have been talking in Klingon!

Misunderstandings and Misadventures

Beside my T-Bill fiasco, there was that time I handed out flyers about interest rates at the local park. I thought I’d take my finance knowledge to the streets, but instead of intrigued investors, I attracted a flock of confused ducks. When I tried to explain why interest rates matter, they quacked in protest, which was perhaps their way of saying, “Too much talk, more bread!”

When I finally realised the ducks were more interested in bread than bonds, I couldn’t help but laugh at the absurdity. It seems trying to enlighten a group of quacking waterfowl about financial literacy wasn’t my best idea! I walked away with soggy flyers and a newfound respect for ducks. Who knew they had such strong opinions on economic matters? They certainly made my speech one quack-tastic adventure!

Tips for Future T-Bill Investors

Despite the bumpy ride that T-bill rates often seem to take, there are some golden nuggets of wisdom I’ve learnt along the way. Here’s what I’d suggest for anyone eyeing these little gems:

- Stay updated on market trends.

- Diversify your investment portfolio.

- Start with short-term T-bills before diving deeper.

- Keep an eye on inflation rates.

The right approach could turn your T-bills into a treasure trove!

What I Wish I Knew Before Investing

Below, I’ll share a couple of realisations that could save you from the pitfalls I stumbled into. For instance, I wish I had known about the importance of understanding the yield curve better. It’s one of those concepts that sounds fancy until you discover it can seriously impact your returns. If only I had paid more attention during my economics classes!

Encouraging a Sense of Humor in Finance

One thing I’ve picked up is that a good chuckle can help ease the tension surrounding money matters. If you find yourself knee-deep in complex charts and abysmal projections, just remember—if the market was a person, it would definitely be the unpredictable friend who forgets your birthday yet shows up at the pub with cake!

Another interesting takeaway is how humour often helps in making financial discussions less daunting. I’ve found that sharing a light-hearted joke about my earlier investing blunders with friends brings a wave of laughter, making us all feel a bit more at ease with our own financial follies. So go ahead and laugh at that time I thought I could day-trade like a pro—there’s nothing like a bit of levity to bond over the strange, yet fascinating world of finance!

Final Words

Considering all points, I can’t help but chuckle at how the interest rates for T-bills took a nosedive. Just when I thought I’d be rolling in the dough with my 6-month T-bill at a staggering 27%, life threw me a curveball! It’s like my old mate Bob, who, when trying to impress a date, ended up tripping over his shoelaces. T-bill rates can be as unpredictable as my attempts at gourmet cooking. So, whether you’re investing or cooking, just know that sometimes, it’s all a bit of a gamble!

FAQ

Q: Why did T-Bill interest rates drop recently?

A: The recent drop in T-Bill interest rates can largely be attributed to shifts in economic confidence and central bank policies. With inflation showing signs of stabilising and expectations of a potential economic slowdown, investors are seeking safer investments, resulting in increased demand for T-Bills. It’s like when you’re at a party and the pizza arrives—it doesn’t matter that the host only have plain cheese; suddenly, everyone wants a slice! In my case, I found myself trying to convince my colleague, who claimed to be on a diet, to join me for a midnight snack. Just like T-Bills, sometimes the safer options become too enticing to resist!

Q: How does the yield on T-Bills affect general savings?

A: When T-Bill yields drop, it might seem like a sad fortune cookie message about your savings; however, it can encourage banks to lower their interest rates as well, ultimately affecting savings accounts. I once opened a savings account with expectations of great interest, only to find out it was less entertaining than watching paint dry! But, as it turns out, T-Bills getting attention can lead banks to have more appealing offers later. Just a reminder: let’s hope those interest rates don’t stay on holiday forever!

Q: Are T-Bills a good investment option with falling interest rates?

A: Absolutely! Falling interest rates can make T-Bills a rather attractive option for risk-averse investors. While returns may be lower than exciting adventures, it’s a stable and safe choice. One time, I decided to invest in stocks, convinced it was my golden ticket to the high life. Spoiler alert: it wasn’t. So, when T-Bill rates dropped, I kept my portfolio simple like a slice of toast with butter. Sometimes simple is the best bet when it comes to saving for the future!

Q: What should investors look for when T-Bill rates are changing?

A: When T-Bill rates change, it’s crucial for investors to look at the economic indicators and trends. Keeping an eye on inflation rates and central bank announcements can help determine future movements. I once tuned in to a financial news broadcast, thinking I would hear whispers of excitement, only to learn it was just someone talking about the weather in the stock market! Pay attention and you might just spot a trend before it leaps out at you like the cat that suddenly appears from nowhere. Be prepared, and you’ll be one step ahead of the game!

Q: Can I still benefit from T-Bills with current yields?

A: Indeed! While current yields may not be as thrilling as watching your favourite TV drama (or perhaps as thrilling as an episode of “The Office”), T-Bills can offer a dependable return. Personally, I compare investing in T-Bills to binge-watching a familiar series: it might not give you the instant dopamine rush but offers a sense of security until you find that next big blockbuster. So go ahead, settle in with those T-Bills like an old sitcom—you might find comfort in their reliable nature!